UPDATED JUNE 16, 2013

Mobile Finance is big and getting bigger, with close to 52.M people or 34% of all US wireless subscribers accessing their bank information via a mobile device in Q4 2012. comScore estimates a 21% increase in mobile banking overall and an eye-popping 45% increase in mobile banking app usage since Q4 of 2011.

Obviously this increase in SMS text, mobile browser and app usage is a boon to the banks and credit card companies as they look to move expensive customer service channels to automated self service. But so far, mobile banking is focused on basic account servicing capabilities to address core customer needs like balance, payment and transfers.

This is changing, however, as the amount of payments in the mobile and online space grows past $6BN at a accelerating rate. Potential disruptors to old school banking like Paypal, Serve, and Google wallet seek to redefine payments without shaking the boat on the industry’s revered merchant fee profit model. More adventurous disruptors like Dwolla are eliminating the merchant fee altogether. As fees and rates become increasingly commoditized, payments companies can compete on superior customer utility and experience to gain dominance in the emerging global digital currency.

The first of a 4 part series, this review compares twelve account management capabilities accross six banks, five payment companies, and one financial account aggregator, mint.com. Following this entry, the next three blogs will investigate the mobile offerings of the same ten companies across 30 capabilities in Information and Education, Payment, and Loyalty categories. Taken altogether, this review will give you a solid foundation of core mobile capabilities in the retail finance industry and a clear understanding of which elements will shape the future competitive marketplace.

I. Account Management

Financial companies have extended most account management functions to the online and mobile space. This makes sense when you think of the compelling and immediate savings of migrating from a cost-per-contact of $5-$8 for the phone and $15-$25 per branch visit to an online/mobile cost per contact of less than $0.25. Simple, high volume transactions like balance inquiry, payment, and transfer functions are all available.

The below chart outlines the availability of eleven core account management transactions for ten financial service and payment companies.

A few account servicing processes are still out of scope for mobile apps. These holdouts are generally more complicated or high security account transactions like dispute a charge, fraud processing, and change of address. Interestingly, apart from Discover and Level Up, initial account set up, activation and password reset still require out-of-app browser or phone interaction which seems an easy target for automization.

What’s most surprising, however, is that there are still a few bank hold-outs (BofA and Discover) thatstill moss one of the most promising mobile based account utilities: remote check acceptance. A recent study conducted by Mercatus found that 43% of responders who use mobile banking would switch banks for the ability to deposit a check by taking a picture of it. Pioneered by USAA, Chase and Paypal were the other early adopters of this super useful functionality and have benefited handsomely with an inflow of new customers like US troops stationed overseas for whom remote deposit is an essential tool.

In the same Mercatus study, a full 50% of customers cited that mobile banking functionality played a role in the decision for their primary bank. Indeed, remote deposit marks a clear milestone in the evolution of value creation for financial services. Original Bricks and Mortar driven thinking focused on the security, deposit base and geographic footprint of a bank as the core decision criteria for doing business. More recently, financial services found excellent customer service as a means of differentiation for customer acquisition and retention. We are now seeing the new wave of competition in Financial Services: Mobile features that create friction free processing anytime anywhere in an intuitive and enriching customer interface.

In this new landscape, Security is likely to become the next frontier. Believe what you want about the potential risks of NFC and other mobile technologies. the simple reality is that the most fallible security structure is the ubiquitous password. Of note in this space, Bof A offers an additional dynamic PIN security layer and Level Up enables a PIN lock.

So far the competitive landscape for mobile banking is wide open for a dominant move that leverages more of the benefits of mobile to significantly enhance customer utility and drive loyalty as part of the experience.

In the next blog entry we will review the Information and Education category and see how some industry leaders are making early moves to using uniquely mobile features as a source of value enrichment for their customers and a key part of the new competitive landscape.

Banks and Payment mobile apps are just beginning to go beyond basic account information. Early wins in customer adoption of Account Disclosures and Branch /ATM locations to their mobile customers are leading to a few companies creating and curating branded financial information and education to enrich the customer utility and increase engagement. This blog looks at five informational capabilities financial companies will employ to compete for mobile dominance and describe key success factors that will define the winners.

II. INFORMATION IS POWER

*AmEx hosts most of its education on separate sites like the OPEN Forum, Citi content is reserved for ipad app.

1. Disclosures are a win-win

All of the ten companies reviewed provide basic account terms and disclosures. This is because of the multiple benefits from a compliance and cost perspective. Recent US regulations make the ability to manage the presentment of account terms a key compliance requirement, with explicit restrictions on how often account terms can change and the ability for a customer to opt in or out. Mobile customers are already comfortable with regular app updates and the mobile interface enables a company to get an explicit opt in/out. Add to that the very real opportunity to avoid the $0.50+ per mailing cost for the thick and intimidating paper version and you can see why this was the first informational element to be adopted on the mobile browser and apps.

2. Mobile Information Finds Value

Another great feature is the find a Branch /ATM location. Relevant and timely information that leverages mobility to deliver incremental value to the customer. But why stop there? What about merchants that accept the card or payment device? As flattering or cool as it is to use your Centurion card or your Dwolla tap, these only work if the merchant accepts it. Break down in the sticks near a cash-only garage and you, the issuer, and the merchant are all s--- out of luck. Its a welcome development, therefore, for Level Up and Dwolla to include a "Find Merchants that Accept" near you (the screenshot to the right shows 2 Dwolla merchants in a 15 mile radius of my house). While this is not something AmEx wants to make its users think about, it definitely would be useful in foreign countries and rural areas where the blue box window sticker is harder to find.

Another great feature is the find a Branch /ATM location. Relevant and timely information that leverages mobility to deliver incremental value to the customer. But why stop there? What about merchants that accept the card or payment device? As flattering or cool as it is to use your Centurion card or your Dwolla tap, these only work if the merchant accepts it. Break down in the sticks near a cash-only garage and you, the issuer, and the merchant are all s--- out of luck. Its a welcome development, therefore, for Level Up and Dwolla to include a "Find Merchants that Accept" near you (the screenshot to the right shows 2 Dwolla merchants in a 15 mile radius of my house). While this is not something AmEx wants to make its users think about, it definitely would be useful in foreign countries and rural areas where the blue box window sticker is harder to find.

3. News: The Early Edition

Financial News and Articles are more recent additions to the mobile experience, with Citibank's ipad app an early leader in providing a fully integrated experience. AmEx has some good links to the OPEN Forum and additional educational sites for consumers, but these have limited targeting beyond the entrepreneur and thus far can only be accessed through a link to the mobile browser, bringing the customer out of the app and away from their profile. More targeted information that the customer can curate themselves through Likes and dislikes would work better.

4. Financial U

Citibank, Amex and mint.com all provide some decent links and articles on financial responsibility, understanding APRs, and tips to encourage fiscal responsibility. I’ve also heard some good things about the “Talk to Chuck App” from Charles Schwab but I had to draw the line somewhere in terms of how many personal accounts I set up for the purposes of this review.

5. Know Thyself to Enrich Thyself

What I’m most excited about is the opportunity to inform and educate consumers on their actual account and spend information. This has huge benefits for both consumers and the companies they transact with. Here's how:

Consumers: Most of the apps reviewed enable the user to sort account information by categories like date, account, and spend category. The dashboards available provide a solid tool for customers to understand their relationships with that one bank or payment provider.

But who does all their activity with just one company? Creditcards.com estimates that 80% of Americans hold a debit card and that the average card holder has 3.5 credit cards in their wallet. For those of us with 5 or more active accounts in play, mint.com takes the prize for its ability to aggregate account information like balance, payment due dates, and your actual spend by category for every account you load. Once you get past the initial shock of seeing how much you really spend in bars, restaurants, and coffee shops, you will find mint.com provides a simple and effective interface to gather and display your data to encourage better fiscal discipline and avoid unnecessary fees. The mint.com advice section promises to proactively suggest ways to reduce account fees and optimize investments but so far the tool has limited ability and couldn’t offer one recommendations for me.

Companies:

The company that can access the complete view of your financial profile and spend behavior has the best opportunity to provide hyper-relevant offers across a wide span of financial investment, loan, and insurance products. Not only do they know what you need, they know when you need it and are capable of providing instant and immediate access with real-time and geographic identification, eligibility, and pricing.

We will dig deeper into the ability to make offers in the final section of this Mobil Banking Apps review on Loyalty. In the third section on Payments coming next, look for the explosive power of linking information on spend and budget with actual payment controls

III. Payments Functionality still lags for Mobile Banking Apps

While information is power, money makes the world go around. Dominance in the Digital Payments industry is one logical objective for financial apps as it is believed that the company that controls the money flow is in the best position to control the transaction fees and the customer purchase data. Armed with the cash and the data, the winning payments company will be well funded and have unmatched information on how to best cater and price to customer needs.

This is even more critical when one considers Gartner’s estimates that 200 MM consumers used mobile payments globally in 2012. Beyond what is currently spent on credit and debit cards, the biggest prize is spend in cash and checks. Make a better payment process and there is a huge opportunity to capture the lion’s share of that space within one lifetime.

This is even more critical when one considers Gartner’s estimates that 200 MM consumers used mobile payments globally in 2012. Beyond what is currently spent on credit and debit cards, the biggest prize is spend in cash and checks. Make a better payment process and there is a huge opportunity to capture the lion’s share of that space within one lifetime.

In the below comparison we can see how mobile apps of our ten financial companies stack up on five payments capabilities.

*Peer must be on network or have account w same company.

*Peer must be on network or have account w same company.

**Citibank bump to pay enabled by Google Wallet in test markets

Mint.com doesn’t pay. While I love how mint.com makes it easy to see all my accounts in one place, it’s always going to play a second act to the companies that actually enable payments. As an account information aggregator, mint.com makes money on advertising and click-through fees related to offers and advice. Therefore, mint.com’s long term utility is based on the hope that no one financial payments company gains dominance and that the mobile interface for financial apps continues to leave room for an information aggregator. Such hopes may be short lived.

Banks lag in Social Payment functions. Banks are slower to offer advanced payment features. The banks and AmEx mobile apps have not yet embraced all of the possible payments functionality that currently differentiate the upstarts like PayPal, Google Wallet, Dwolla and Serve (Serve is owned by AmEx). This is changing, however, with Citi, Chase, and Discover enabling Peer to Peer exchange. More social payment options like split the bill and fundraising remain the domain of the payments companies for now. The banks may well consider taking from AmEx's Serve playbook by adding these functions in a plan to attract younger and more socially active customer groups.

Why is Pay Later so late? One potent opportunity in the payments space remains out of reach for the ten mobile apps reviewed in this blog: delayed payments. Inherent in a credit card structure is the ability to purchase now and be billed upon the statement close. According to the 2010 US Census Bureau, the average American credit card holder owes $5,100 in credit card debt.

Why is Pay Later so late? One potent opportunity in the payments space remains out of reach for the ten mobile apps reviewed in this blog: delayed payments. Inherent in a credit card structure is the ability to purchase now and be billed upon the statement close. According to the 2010 US Census Bureau, the average American credit card holder owes $5,100 in credit card debt.

If that’s true, then it stands to reason that if customers are making mobile purchases, they should also be able to indicate what items they can/will pay for now and which purchases they want to defer. Depending on the structure, both the merchant and the payment company are in a position to offer payment terms with the potential for substantial profits from on-the-spot lending functionality.

A few companies like Bill Me Later (owned by Ebay who also owns PayPal) do offer this functionality. As such, it’s probably a matter of time until mainstream mobile apps also allow you the option to delay payment on that Superbowl TVpurchase until long after the game. Another great way to support consumer’s penchant for debt as outlined in this infographic of the customer debt lifecycle:

NFC not near enough. NFC or near field communications is still in early stages. While the decision by 45 different carriers to adopt NFC is a great step forward, only a few of the devices or payment companies currently offer the ability to pay at the register with a wave of the phone. Worse, while it is more convenient than cash, NFC saves very little time from a traditional credit or debit card swipe. By the time you take out your phone, put in the device password, bring up your payment app and finally put in the payment app password, you could have swiped your card, bagged the item and walked out the door.

The case for NFC will change, however, as the merchant side gets more sophisticated in leveraging NFC to recognize and reward individual customers with customized offers based on the customer location. ABI Research believes that 85 per cent of all new point of sale terminals shipped in 2016 will be NFC-enabled. And Strategy Analytics forecasts there will be $50 billion in mobile transactions made and 1.5 billion handsets sold between 2010 and 2016 with SIM-based NFC capabilities worldwide.

In all, mobile app enabled Payments is expected to see a lot more action in the coming years. Look for traditional bank and credit card companies leverage their mobile apps to keep their market share while capturing more cash and check payments digitally. At the same time, newer mobile payment entrants look to revolutionize the payment process altogether. We will look at how these companies are using loyalty features in their apps to compete for customers and the ability to own the payments experience.

IV. Banking Payment Apps: Loyalty Will Lead

At the far end of the banking and payment apps maturity curve waits Loyalty based functionality. A unique blend of brand awareness, emotional connection, and enticing content, Loyalty is what transcends the pure functionality of account management and payments into an emotional glue. This glue enriches the customer connection and increases company profitability. The final of four entries, this section will review our twelve companies against 8 Loyalty capabilities including Offers, Rewards, and Social Media.

* Still in Geographic pilot, CapOne says they have a robust deals program, but dont have it in the backwoods area of New York City yet.

* Still in Geographic pilot, CapOne says they have a robust deals program, but dont have it in the backwoods area of New York City yet.

Ad Free, for now: Thus far, none of the true bank and payment apps show third party advertisements on their apps. As mentioned before, Mint.com is the exception since it is an information aggregator and ads are its prime revenue model. That said, if it can work for a Mint.com, it is not inconceivable to imagine a low-frills bank option that shows ads in return for free checking or other perks. Most apps in other categories use the same approach so it is not a stretch to consider it in banking and payment.

Really, no Account Benefits? By far the biggest gap I identified in all four sections of this review is the almost complete lack of product benefit information. Most credit cards and even debit cards come with some package of benefits like extended warranty, fraud protection, discounts with co-branded partners or limited rental car insurance. You probably accepted a costly acquisition offer because of these benefits. But now the company has spent all this money to acquire you, do they really want you to forget about the same features that prompted you to sign up? At least LevelUp provides a pictorial representation of how and why to use it. Also noteworthy is Discover which does a good job of promoting its cashback and accelerated points programs.

Really, no Account Benefits? By far the biggest gap I identified in all four sections of this review is the almost complete lack of product benefit information. Most credit cards and even debit cards come with some package of benefits like extended warranty, fraud protection, discounts with co-branded partners or limited rental car insurance. You probably accepted a costly acquisition offer because of these benefits. But now the company has spent all this money to acquire you, do they really want you to forget about the same features that prompted you to sign up? At least LevelUp provides a pictorial representation of how and why to use it. Also noteworthy is Discover which does a good job of promoting its cashback and accelerated points programs.

Since these benefits can cost money to fulfill, it’s easy to imagine why some companies would purposely avoid reminding you of them. But this thinking is penny wise and pound foolish. In the 2011 JD Powers US Credit Card study, customers of the 5 in a row winner, American Express, could recall 3.4 product benefits as compared with the industry average of 1.3 benefits recalled. Discover was the next closest. It is therefore no surprise that American Express and Discover are the only companies reviewed that reminds app users of the many benefits related to their specific products.

No Prizes and No Fun: One thing that’s clear from the apps reviewed: finance and payments are all business and no play. Unlike mobile carrier apps, Contests and Giveaways are completely absent. So too are relevant local Events missing from most of the apps reviewed. How boring! For some reason many companies believe they can just convince me to change my behavior for their benefit (think turning off paper statements or ceasing to make payments over the phone) without some type of enticement. Sooner or later banks are going to realize you catch more bees with honey than vinegar.

Location Based Offers Are Here: Offers for discounts or double points triggered by your location are a key differentiator for the payment apps compared with the banking apps. While still limited in the number of merchants that actually accept them, payment companies are jumping into the estimated $1BN market for daily and location based deals currently dominated by Groupon and Living Social (estimate provided by BIAKelsey Analysts. Click here for a cool infographic on the hyperbolic growth of this industry).

Done correctly, this would be a huge win for all parties. The customer gets a thrill and a discount. The merchant can leverage advanced segmentation capabilities based on rich customer data from the bank/ payment company to target specific deals and drive more profitable traffic than Groupon can. Finally the bank or payment company gets loyal customers and profits from the discount rate on their increased spend. AmEx, Chase, B of A, and Capital One are early innovators in the space, although I've been deeply disappointed in the program offerings to date from all of these companies.

Done correctly, this would be a huge win for all parties. The customer gets a thrill and a discount. The merchant can leverage advanced segmentation capabilities based on rich customer data from the bank/ payment company to target specific deals and drive more profitable traffic than Groupon can. Finally the bank or payment company gets loyal customers and profits from the discount rate on their increased spend. AmEx, Chase, B of A, and Capital One are early innovators in the space, although I've been deeply disappointed in the program offerings to date from all of these companies.

Don’t you Want to Cross Sell me? Because I used to work in the cross sell side of the credit card business, I am keenly aware of how profitable making relevant upsell offers to existing customers on the phone. Banks and Credit card companies are going to wake up soon and realize they have been too successful in driving transactions to the web and mobile and miss the cross sell revenue they have become accustomed to. At that time, we will see more interest in adding offers for upgraded products, additional cards, insurance, and other product extensions. For now, BofA and Capital One do the best job of offering alternative card products, with AmEx and Discover stuck in low gear with member get member programs. At this point, Mint does the best job of aggregating your profile to offer relevant financial products on the widest spectrum.

Don’t you Want to Cross Sell me? Because I used to work in the cross sell side of the credit card business, I am keenly aware of how profitable making relevant upsell offers to existing customers on the phone. Banks and Credit card companies are going to wake up soon and realize they have been too successful in driving transactions to the web and mobile and miss the cross sell revenue they have become accustomed to. At that time, we will see more interest in adding offers for upgraded products, additional cards, insurance, and other product extensions. For now, BofA and Capital One do the best job of offering alternative card products, with AmEx and Discover stuck in low gear with member get member programs. At this point, Mint does the best job of aggregating your profile to offer relevant financial products on the widest spectrum.

Rewards are Still Just Point Values: Only banks and credit card offer rewards so this section only applies to them. That said, most rewards information is just a simple reward balance. Only AmEx, Discover, Chase and Cap1 provide redemption opportunities. For a program that is designed to instill loyalty, these mobile apps fail to impress. It would be great to be able to use my reward points for actual in-person purchases. Or get special points bonuses for using my card at some combination of merchants or categories (think consumer based scavenger hunt a la foursquare)

How Social is your Payments App? Sure all of these companies have a Facebook presence, but not all of them enable you to reach it through their apps. This is an immediate opportunity for companies to encourage app usage and create greater linkage between their many faces and a single customer interface. But aren’t your finances a personal affair? The details of your actual balances and activity may be, but if the goal is to instill loyalty and repeat usage, finance apps need to do a better job of transcending this perceived barrier and finding ways for customers to link with their social networks to deliver greater stickiness and value.

How Social is your Payments App? Sure all of these companies have a Facebook presence, but not all of them enable you to reach it through their apps. This is an immediate opportunity for companies to encourage app usage and create greater linkage between their many faces and a single customer interface. But aren’t your finances a personal affair? The details of your actual balances and activity may be, but if the goal is to instill loyalty and repeat usage, finance apps need to do a better job of transcending this perceived barrier and finding ways for customers to link with their social networks to deliver greater stickiness and value.

In summary, Mobile Banking and Payment Apps are still a long way from reaching their potential. More of an extension of tradition bricks and mortar functionality, they have been successful at shifting service volume from high cost to lower cost channels. In the process, however, banks and payment companies are waking up to the fact that the mobile app functionality is the competitive landscape.

In the foreseeable future there will be no reason a customer must to go to a physical location for their banking and payment needs. Its here where the established banks have the most to lose, since this shakes the very foundations of competitiveness that defined historical banking: deposits, locations, and fees. Instead, the convenience and added benefits of geolocation, information aggregation, deals, and loyalty creates a new playing rich with opportunities for winning companies to create incremental customer and shareholder value. This is where the Credit Unions and smaller banks can gain ground and compete with the banking Goliaths, armed with lower rates, customer-centric service and an app in a sling.

Mobile Finance is big and getting bigger, with close to 52.M people or 34% of all US wireless subscribers accessing their bank information via a mobile device in Q4 2012. comScore estimates a 21% increase in mobile banking overall and an eye-popping 45% increase in mobile banking app usage since Q4 of 2011.

Obviously this increase in SMS text, mobile browser and app usage is a boon to the banks and credit card companies as they look to move expensive customer service channels to automated self service. But so far, mobile banking is focused on basic account servicing capabilities to address core customer needs like balance, payment and transfers.

This is changing, however, as the amount of payments in the mobile and online space grows past $6BN at a accelerating rate. Potential disruptors to old school banking like Paypal, Serve, and Google wallet seek to redefine payments without shaking the boat on the industry’s revered merchant fee profit model. More adventurous disruptors like Dwolla are eliminating the merchant fee altogether. As fees and rates become increasingly commoditized, payments companies can compete on superior customer utility and experience to gain dominance in the emerging global digital currency.

The first of a 4 part series, this review compares twelve account management capabilities accross six banks, five payment companies, and one financial account aggregator, mint.com. Following this entry, the next three blogs will investigate the mobile offerings of the same ten companies across 30 capabilities in Information and Education, Payment, and Loyalty categories. Taken altogether, this review will give you a solid foundation of core mobile capabilities in the retail finance industry and a clear understanding of which elements will shape the future competitive marketplace.

I. Account Management

Financial companies have extended most account management functions to the online and mobile space. This makes sense when you think of the compelling and immediate savings of migrating from a cost-per-contact of $5-$8 for the phone and $15-$25 per branch visit to an online/mobile cost per contact of less than $0.25. Simple, high volume transactions like balance inquiry, payment, and transfer functions are all available.

The below chart outlines the availability of eleven core account management transactions for ten financial service and payment companies.

What’s most surprising, however, is that there are still a few bank hold-outs (BofA and Discover) thatstill moss one of the most promising mobile based account utilities: remote check acceptance. A recent study conducted by Mercatus found that 43% of responders who use mobile banking would switch banks for the ability to deposit a check by taking a picture of it. Pioneered by USAA, Chase and Paypal were the other early adopters of this super useful functionality and have benefited handsomely with an inflow of new customers like US troops stationed overseas for whom remote deposit is an essential tool.

In the same Mercatus study, a full 50% of customers cited that mobile banking functionality played a role in the decision for their primary bank. Indeed, remote deposit marks a clear milestone in the evolution of value creation for financial services. Original Bricks and Mortar driven thinking focused on the security, deposit base and geographic footprint of a bank as the core decision criteria for doing business. More recently, financial services found excellent customer service as a means of differentiation for customer acquisition and retention. We are now seeing the new wave of competition in Financial Services: Mobile features that create friction free processing anytime anywhere in an intuitive and enriching customer interface.

In this new landscape, Security is likely to become the next frontier. Believe what you want about the potential risks of NFC and other mobile technologies. the simple reality is that the most fallible security structure is the ubiquitous password. Of note in this space, Bof A offers an additional dynamic PIN security layer and Level Up enables a PIN lock.

So far the competitive landscape for mobile banking is wide open for a dominant move that leverages more of the benefits of mobile to significantly enhance customer utility and drive loyalty as part of the experience.

In the next blog entry we will review the Information and Education category and see how some industry leaders are making early moves to using uniquely mobile features as a source of value enrichment for their customers and a key part of the new competitive landscape.

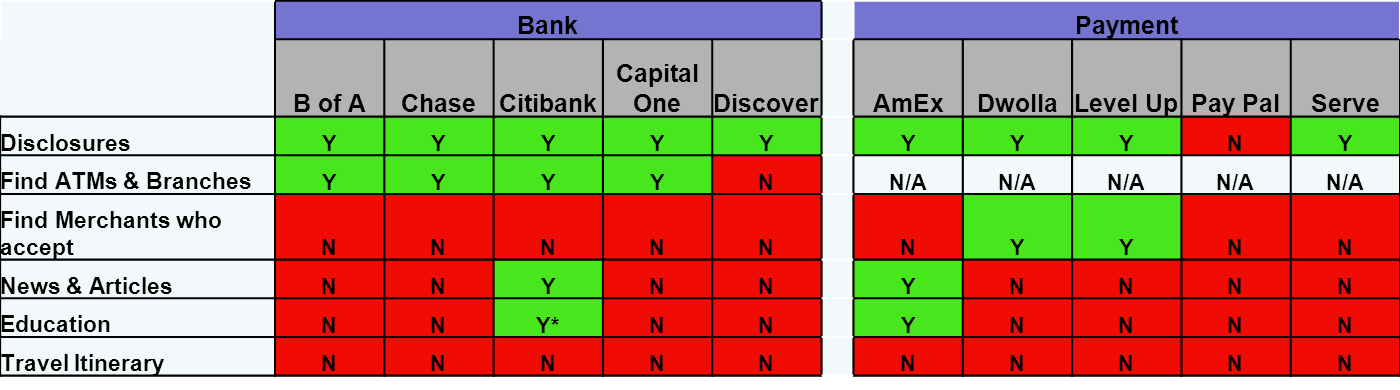

Banks and Payment mobile apps are just beginning to go beyond basic account information. Early wins in customer adoption of Account Disclosures and Branch /ATM locations to their mobile customers are leading to a few companies creating and curating branded financial information and education to enrich the customer utility and increase engagement. This blog looks at five informational capabilities financial companies will employ to compete for mobile dominance and describe key success factors that will define the winners.

II. INFORMATION IS POWER

*AmEx hosts most of its education on separate sites like the OPEN Forum, Citi content is reserved for ipad app.

1. Disclosures are a win-win

All of the ten companies reviewed provide basic account terms and disclosures. This is because of the multiple benefits from a compliance and cost perspective. Recent US regulations make the ability to manage the presentment of account terms a key compliance requirement, with explicit restrictions on how often account terms can change and the ability for a customer to opt in or out. Mobile customers are already comfortable with regular app updates and the mobile interface enables a company to get an explicit opt in/out. Add to that the very real opportunity to avoid the $0.50+ per mailing cost for the thick and intimidating paper version and you can see why this was the first informational element to be adopted on the mobile browser and apps.

2. Mobile Information Finds Value

Another great feature is the find a Branch /ATM location. Relevant and timely information that leverages mobility to deliver incremental value to the customer. But why stop there? What about merchants that accept the card or payment device? As flattering or cool as it is to use your Centurion card or your Dwolla tap, these only work if the merchant accepts it. Break down in the sticks near a cash-only garage and you, the issuer, and the merchant are all s--- out of luck. Its a welcome development, therefore, for Level Up and Dwolla to include a "Find Merchants that Accept" near you (the screenshot to the right shows 2 Dwolla merchants in a 15 mile radius of my house). While this is not something AmEx wants to make its users think about, it definitely would be useful in foreign countries and rural areas where the blue box window sticker is harder to find.3. News: The Early Edition

Financial News and Articles are more recent additions to the mobile experience, with Citibank's ipad app an early leader in providing a fully integrated experience. AmEx has some good links to the OPEN Forum and additional educational sites for consumers, but these have limited targeting beyond the entrepreneur and thus far can only be accessed through a link to the mobile browser, bringing the customer out of the app and away from their profile. More targeted information that the customer can curate themselves through Likes and dislikes would work better.

4. Financial U

Citibank, Amex and mint.com all provide some decent links and articles on financial responsibility, understanding APRs, and tips to encourage fiscal responsibility. I’ve also heard some good things about the “Talk to Chuck App” from Charles Schwab but I had to draw the line somewhere in terms of how many personal accounts I set up for the purposes of this review.

5. Know Thyself to Enrich Thyself

What I’m most excited about is the opportunity to inform and educate consumers on their actual account and spend information. This has huge benefits for both consumers and the companies they transact with. Here's how:

Consumers: Most of the apps reviewed enable the user to sort account information by categories like date, account, and spend category. The dashboards available provide a solid tool for customers to understand their relationships with that one bank or payment provider.

But who does all their activity with just one company? Creditcards.com estimates that 80% of Americans hold a debit card and that the average card holder has 3.5 credit cards in their wallet. For those of us with 5 or more active accounts in play, mint.com takes the prize for its ability to aggregate account information like balance, payment due dates, and your actual spend by category for every account you load. Once you get past the initial shock of seeing how much you really spend in bars, restaurants, and coffee shops, you will find mint.com provides a simple and effective interface to gather and display your data to encourage better fiscal discipline and avoid unnecessary fees. The mint.com advice section promises to proactively suggest ways to reduce account fees and optimize investments but so far the tool has limited ability and couldn’t offer one recommendations for me.

Companies:

The company that can access the complete view of your financial profile and spend behavior has the best opportunity to provide hyper-relevant offers across a wide span of financial investment, loan, and insurance products. Not only do they know what you need, they know when you need it and are capable of providing instant and immediate access with real-time and geographic identification, eligibility, and pricing.

We will dig deeper into the ability to make offers in the final section of this Mobil Banking Apps review on Loyalty. In the third section on Payments coming next, look for the explosive power of linking information on spend and budget with actual payment controls

III. Payments Functionality still lags for Mobile Banking Apps

While information is power, money makes the world go around. Dominance in the Digital Payments industry is one logical objective for financial apps as it is believed that the company that controls the money flow is in the best position to control the transaction fees and the customer purchase data. Armed with the cash and the data, the winning payments company will be well funded and have unmatched information on how to best cater and price to customer needs.

In the below comparison we can see how mobile apps of our ten financial companies stack up on five payments capabilities.

**Citibank bump to pay enabled by Google Wallet in test markets

Mint.com doesn’t pay. While I love how mint.com makes it easy to see all my accounts in one place, it’s always going to play a second act to the companies that actually enable payments. As an account information aggregator, mint.com makes money on advertising and click-through fees related to offers and advice. Therefore, mint.com’s long term utility is based on the hope that no one financial payments company gains dominance and that the mobile interface for financial apps continues to leave room for an information aggregator. Such hopes may be short lived.

Banks lag in Social Payment functions. Banks are slower to offer advanced payment features. The banks and AmEx mobile apps have not yet embraced all of the possible payments functionality that currently differentiate the upstarts like PayPal, Google Wallet, Dwolla and Serve (Serve is owned by AmEx). This is changing, however, with Citi, Chase, and Discover enabling Peer to Peer exchange. More social payment options like split the bill and fundraising remain the domain of the payments companies for now. The banks may well consider taking from AmEx's Serve playbook by adding these functions in a plan to attract younger and more socially active customer groups.

If that’s true, then it stands to reason that if customers are making mobile purchases, they should also be able to indicate what items they can/will pay for now and which purchases they want to defer. Depending on the structure, both the merchant and the payment company are in a position to offer payment terms with the potential for substantial profits from on-the-spot lending functionality.

A few companies like Bill Me Later (owned by Ebay who also owns PayPal) do offer this functionality. As such, it’s probably a matter of time until mainstream mobile apps also allow you the option to delay payment on that Superbowl TVpurchase until long after the game. Another great way to support consumer’s penchant for debt as outlined in this infographic of the customer debt lifecycle:

NFC not near enough. NFC or near field communications is still in early stages. While the decision by 45 different carriers to adopt NFC is a great step forward, only a few of the devices or payment companies currently offer the ability to pay at the register with a wave of the phone. Worse, while it is more convenient than cash, NFC saves very little time from a traditional credit or debit card swipe. By the time you take out your phone, put in the device password, bring up your payment app and finally put in the payment app password, you could have swiped your card, bagged the item and walked out the door.

The case for NFC will change, however, as the merchant side gets more sophisticated in leveraging NFC to recognize and reward individual customers with customized offers based on the customer location. ABI Research believes that 85 per cent of all new point of sale terminals shipped in 2016 will be NFC-enabled. And Strategy Analytics forecasts there will be $50 billion in mobile transactions made and 1.5 billion handsets sold between 2010 and 2016 with SIM-based NFC capabilities worldwide.

In all, mobile app enabled Payments is expected to see a lot more action in the coming years. Look for traditional bank and credit card companies leverage their mobile apps to keep their market share while capturing more cash and check payments digitally. At the same time, newer mobile payment entrants look to revolutionize the payment process altogether. We will look at how these companies are using loyalty features in their apps to compete for customers and the ability to own the payments experience.

IV. Banking Payment Apps: Loyalty Will Lead

At the far end of the banking and payment apps maturity curve waits Loyalty based functionality. A unique blend of brand awareness, emotional connection, and enticing content, Loyalty is what transcends the pure functionality of account management and payments into an emotional glue. This glue enriches the customer connection and increases company profitability. The final of four entries, this section will review our twelve companies against 8 Loyalty capabilities including Offers, Rewards, and Social Media.

Really, no Account Benefits? By far the biggest gap I identified in all four sections of this review is the almost complete lack of product benefit information. Most credit cards and even debit cards come with some package of benefits like extended warranty, fraud protection, discounts with co-branded partners or limited rental car insurance. You probably accepted a costly acquisition offer because of these benefits. But now the company has spent all this money to acquire you, do they really want you to forget about the same features that prompted you to sign up? At least LevelUp provides a pictorial representation of how and why to use it. Also noteworthy is Discover which does a good job of promoting its cashback and accelerated points programs.

Really, no Account Benefits? By far the biggest gap I identified in all four sections of this review is the almost complete lack of product benefit information. Most credit cards and even debit cards come with some package of benefits like extended warranty, fraud protection, discounts with co-branded partners or limited rental car insurance. You probably accepted a costly acquisition offer because of these benefits. But now the company has spent all this money to acquire you, do they really want you to forget about the same features that prompted you to sign up? At least LevelUp provides a pictorial representation of how and why to use it. Also noteworthy is Discover which does a good job of promoting its cashback and accelerated points programs. Since these benefits can cost money to fulfill, it’s easy to imagine why some companies would purposely avoid reminding you of them. But this thinking is penny wise and pound foolish. In the 2011 JD Powers US Credit Card study, customers of the 5 in a row winner, American Express, could recall 3.4 product benefits as compared with the industry average of 1.3 benefits recalled. Discover was the next closest. It is therefore no surprise that American Express and Discover are the only companies reviewed that reminds app users of the many benefits related to their specific products.

No Prizes and No Fun: One thing that’s clear from the apps reviewed: finance and payments are all business and no play. Unlike mobile carrier apps, Contests and Giveaways are completely absent. So too are relevant local Events missing from most of the apps reviewed. How boring! For some reason many companies believe they can just convince me to change my behavior for their benefit (think turning off paper statements or ceasing to make payments over the phone) without some type of enticement. Sooner or later banks are going to realize you catch more bees with honey than vinegar.

Location Based Offers Are Here: Offers for discounts or double points triggered by your location are a key differentiator for the payment apps compared with the banking apps. While still limited in the number of merchants that actually accept them, payment companies are jumping into the estimated $1BN market for daily and location based deals currently dominated by Groupon and Living Social (estimate provided by BIAKelsey Analysts. Click here for a cool infographic on the hyperbolic growth of this industry).

Done correctly, this would be a huge win for all parties. The customer gets a thrill and a discount. The merchant can leverage advanced segmentation capabilities based on rich customer data from the bank/ payment company to target specific deals and drive more profitable traffic than Groupon can. Finally the bank or payment company gets loyal customers and profits from the discount rate on their increased spend. AmEx, Chase, B of A, and Capital One are early innovators in the space, although I've been deeply disappointed in the program offerings to date from all of these companies.

Done correctly, this would be a huge win for all parties. The customer gets a thrill and a discount. The merchant can leverage advanced segmentation capabilities based on rich customer data from the bank/ payment company to target specific deals and drive more profitable traffic than Groupon can. Finally the bank or payment company gets loyal customers and profits from the discount rate on their increased spend. AmEx, Chase, B of A, and Capital One are early innovators in the space, although I've been deeply disappointed in the program offerings to date from all of these companies. Don’t you Want to Cross Sell me? Because I used to work in the cross sell side of the credit card business, I am keenly aware of how profitable making relevant upsell offers to existing customers on the phone. Banks and Credit card companies are going to wake up soon and realize they have been too successful in driving transactions to the web and mobile and miss the cross sell revenue they have become accustomed to. At that time, we will see more interest in adding offers for upgraded products, additional cards, insurance, and other product extensions. For now, BofA and Capital One do the best job of offering alternative card products, with AmEx and Discover stuck in low gear with member get member programs. At this point, Mint does the best job of aggregating your profile to offer relevant financial products on the widest spectrum.

Don’t you Want to Cross Sell me? Because I used to work in the cross sell side of the credit card business, I am keenly aware of how profitable making relevant upsell offers to existing customers on the phone. Banks and Credit card companies are going to wake up soon and realize they have been too successful in driving transactions to the web and mobile and miss the cross sell revenue they have become accustomed to. At that time, we will see more interest in adding offers for upgraded products, additional cards, insurance, and other product extensions. For now, BofA and Capital One do the best job of offering alternative card products, with AmEx and Discover stuck in low gear with member get member programs. At this point, Mint does the best job of aggregating your profile to offer relevant financial products on the widest spectrum.Rewards are Still Just Point Values: Only banks and credit card offer rewards so this section only applies to them. That said, most rewards information is just a simple reward balance. Only AmEx, Discover, Chase and Cap1 provide redemption opportunities. For a program that is designed to instill loyalty, these mobile apps fail to impress. It would be great to be able to use my reward points for actual in-person purchases. Or get special points bonuses for using my card at some combination of merchants or categories (think consumer based scavenger hunt a la foursquare)

In summary, Mobile Banking and Payment Apps are still a long way from reaching their potential. More of an extension of tradition bricks and mortar functionality, they have been successful at shifting service volume from high cost to lower cost channels. In the process, however, banks and payment companies are waking up to the fact that the mobile app functionality is the competitive landscape.

In the foreseeable future there will be no reason a customer must to go to a physical location for their banking and payment needs. Its here where the established banks have the most to lose, since this shakes the very foundations of competitiveness that defined historical banking: deposits, locations, and fees. Instead, the convenience and added benefits of geolocation, information aggregation, deals, and loyalty creates a new playing rich with opportunities for winning companies to create incremental customer and shareholder value. This is where the Credit Unions and smaller banks can gain ground and compete with the banking Goliaths, armed with lower rates, customer-centric service and an app in a sling.